Why Does the World Need Another Early-Stage Fund of Funds?

Lev, our partner at Moses, shared in his post what it feels like to throw yourself into venture capital without the right structure. Too much capital concentrated in too few places. Limited access to the best opportunities. Cash flows that were impossible to predict. It was a lesson most new LPs learn the hard way: venture isn’t just about conviction, it’s about building the right system around that conviction.

That realization is what ultimately brought us together to build Moses Capital. While Lev approached it as a founder-turned-LP, my own experience over the last fifteen years in venture kept pointing to the same conclusion: early-stage investing is both the most rewarding corner of the market and the hardest one to do well.

It’s also the most misunderstood. The very traits that make early-stage venture uncomfortable, such as volatility, illiquidity, limited downside protection, and messy valuations, are the same traits that create outsized outcomes when managed properly.

If you can structure your exposure in a way that turns those drawbacks into guardrails, early-stage venture stops looking like chaos.

Why Venture Is Harder Than It Looks

Most allocators still approach venture with the same mindset they use for private equity or hedge funds, with occasional commitments and heavy reliance on brand names. But venture doesn’t behave that way. The real breakouts don’t always come from the big brand names — they frequently tend to emerge from managers no one’s heard of yet, especially in the earliest stages.

Additionally, the industry itself has outgrown the playbooks of the past. Venture used to be defined by a small set of firms clustered in Silicon Valley. Today, it spans geographies, sectors, and strategies. From AI infrastructure in Paris to fintech in London to climate software in Toronto. Opportunity is everywhere, but so is noise. Knowing which managers can actually turn early promise into enduring outcomes takes far more context than most LPs can build in-house.

That mismatch is what makes early-stage venture so deceptively challenging. The combination of extreme dispersion, rapid global shifts, and the sheer volume of emerging managers makes it hard to navigate casually. Without a dedicated system, LPs risk concentrating in the obvious names, missing the next generation of venture talent, and chasing venture tourists.

And the data shows how unforgiving the asset class can be. We looked at PitchBook performance for more than 700 venture funds with vintages between 10 and 20 years ago, and compared them to the annualized return of the S&P 500.

Looking at this, two things become hard to ignore:

In some vintages, the share of funds that underperformed public equities was massive, showing how often venture capital failed to deliver even relative to broad public markets

The “failure” rate varies widely from year to year, which means timing alone can distort outcomes across the entire market. An allocator without systematic diversification across vintages risks being overexposed at “bad” timing

The other, often unspoken, challenge is access.

Access in venture is not determined by the size of your check. The well-known tier-1 franchises have been closed to new LPs for years. Furthermore, many of the best emerging managers operate similarly: they raise small funds, limit their LP base, typically by partnering only with people they already know. Without those relationships, it is easy to be left out, or worse, to get into a fund only after everyone else has passed. That is the paradox: the best funds, whether established names or the next generation of managers, are designed to be hard to access.

After running Start Fund with Felix and backing more than 400 companies directly, we transitioned into operating roles. We began investing in funds personally, thinking it would allow us to stay involved in the ecosystem with less intensity.

However, we quickly realized that doing it well takes just as much focus as running a direct portfolio: staying close to managers, tracking their portfolios, and reviewing hundreds of funds over time requires significant discipline and attention.

That’s where the Fund of Funds model comes in.

Rationale for Fund of Funds: Are “Fees on Fees” Worth It?

Why does a Fund of Funds model make the most sense in venture capital?

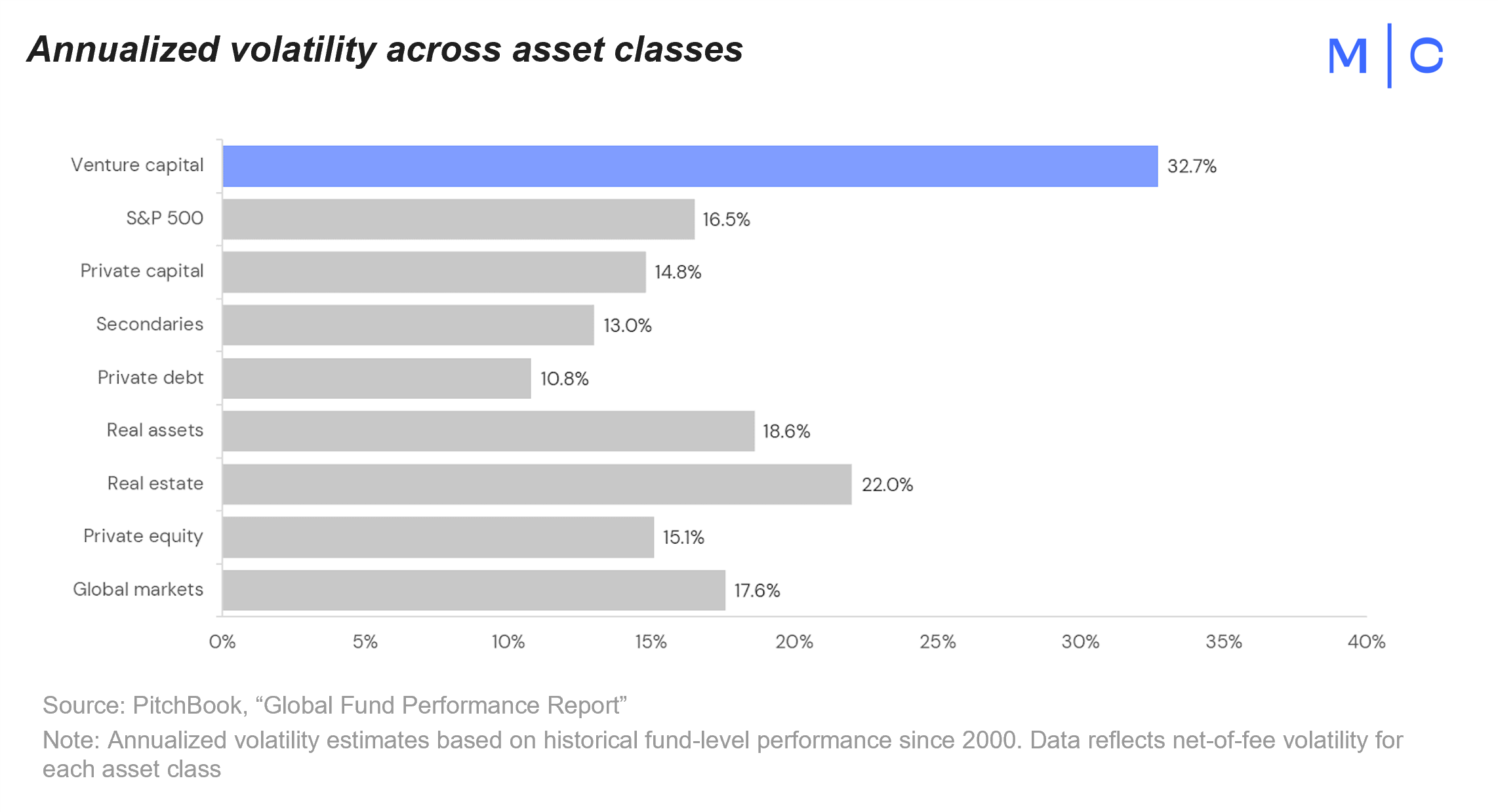

The main reason why Fund of Funds should exist in venture capital at all comes down to volatility. In most private market strategies, dispersion between outcomes is relatively modest. Growth equity, private debt, and even secondaries all show return patterns that cluster fairly tightly. In those categories, layering on an extra fee structure rarely justifies itself, because the upside simply is not wide enough to absorb it.

Venture is different. As PitchBook’s volatility data shows, it is by far the most volatile corner of private markets. The swings are larger, the dispersion between top and bottom quartiles is sharper, and the gap between winners and everyone else is extreme.

In that kind of market, a Fund of Funds structure is not just defensible despite the extra fees; it is uniquely well-suited. The additional layer of cost is outweighed by the value of diversification, access, and systematic exposure. Simply put, venture is probably the only asset class where the payoff curve is steep enough that “fees on fees” can still produce superior outcomes.

Fund of Funds vs VC

In reality, even with the additional fees, venture-focused Fund of Funds have historically performed better than direct VC funds. The common critique is that “fees on fees” leave little upside, but the performance data shows the opposite. In a highly volatile asset class like venture, having a system matters more than fee compression.

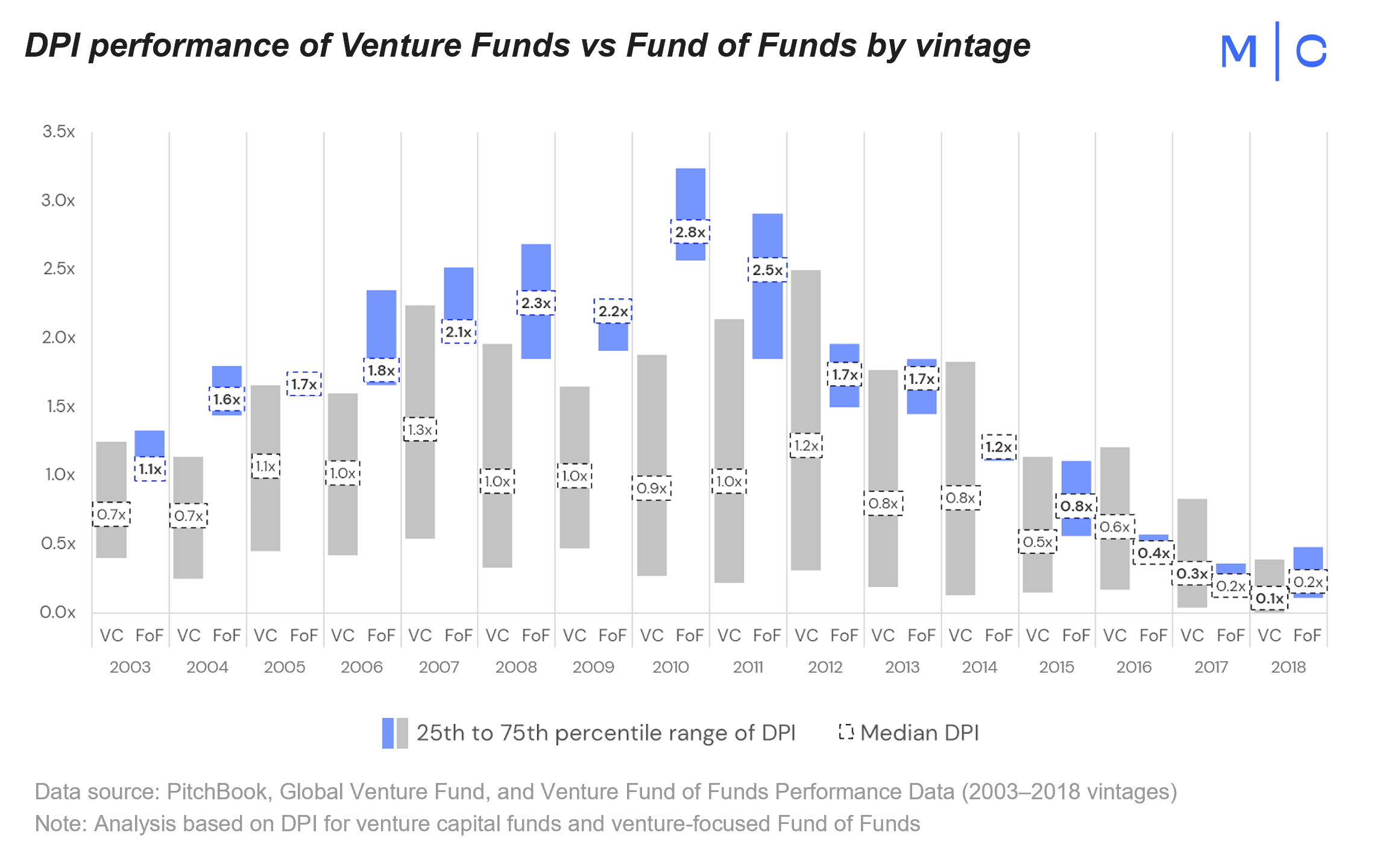

We reviewed 15 years of global VC funds and venture-focused Fund of Funds, looking at vintages that are 7 years or older (the minimum time for money multiples to be meaningful). For comparison, we used net TVPI, which already includes the additional fees charged by Fund of Funds.

In 13 out of 15 vintages, Fund of Funds delivered a higher median net TVPI than direct venture funds

Top-quartile Fund of Funds matched or exceeded top-quartile direct venture funds in 10 of 15 vintages

The downside pattern is even stronger: in every single vintage, the bottom quartile of Fund of Funds outperformed the bottom quartile of direct venture funds

In other words, Fund of Funds consistently protects the downside while still giving investors full exposure to the upside. Not bad for an extra layer of fees.

If TVPI tells one story, DPI makes it even clearer. Over the period we analyzed, the median direct VC fund has often barely returned capital, while Fund of Funds consistently delivered higher distributions and returned capital more reliably.

Why We’re Building Moses

For us, Moses started naturally. As tech investors and founders managing our own capital, we wanted to turn our fund investing into something more durable and consistent.

Over time, it became clear that what we were building could serve others, too. What began as a solution for ourselves grew into a broader platform: a way to give our partners exposure to venture with built-in diversification while saving time and reducing the operational burden.

We built Moses on the belief that early-stage venture capital is too important and complex to approach casually. The world doesn’t need another passive pool of capital. It needs a disciplined system that turns volatility into an advantage, makes access less of a lottery, and gives our investors a practical way to capture venture alpha without getting lost in the noise.

That is the role we set out to play.

| A guest post by

|